Get your business and economy news from the Northern Mariana Islands

Provided by AGPAnfield Energy Demonstrates the Economic Viability of its Hub-And-Spoke Uranium and Vanadium Production Strategy Via Its Updated Preliminary Economic Assessment

Highlights include:

- The updated PEA indicates a pre-tax project internal rate of return (“IRR”) of 106% and a net present value (“NPV”) of US$606 million (with a post-tax IRR of 97% and NPV of $533 million), based on a discount rate of 8% and a uranium price of US$100 per pound, along with a vanadium price of US$9 per pound, with an expected mine and mill capex payback period of 1.3 years.

- Average annual production of approximately 1.3 million pounds of uranium (U3O8) and 6.4 million pounds of vanadium (V2O5) per year is estimated over the 15-year mine life, including a peak production year of 1.9 million pounds of uranium and 7.8 million pounds of vanadium.

- The combined feed of the Velvet-Wood, Slick Rock and the West Slope Mines is designed to meet the increased tonnage capacity at Shootaring of 1,000 tons per day.

- Estimated mill-related capital expenditures at Shootaring, including 20% contingency amount for each item, of: (1) US$31.1 million for general upgrades; (2) US$34.6 million to install a modern vanadium circuit; and (3) US$14.4 million to update the tailings management facility, for a total of US$80.1 million.

- Estimated mine-related capital expenditures, including: (1) engineering and design; (2) mine facilities; (3) mine equipment; (4) the reopening of the decline at Velvet and the sinking of a production shaft at Wood; and (5) the sinking of two production shafts at Slick Rock, with a 10% contingency, of a combined total of US$37.5 million, partially offset by expected cash flow of approximately $23.2 million related to initial uranium production from Anfield’s stockpiled material.

VANCOUVER, British Columbia, May 04, 2026 (GLOBE NEWSWIRE) -- Anfield Energy Inc. (NASDAQ: AEC; TSX.V: AEC; FRANKFURT: 0AD) (“Anfield” or the “Company”) is pleased to report the results of a combined preliminary economic assessment (“PEA”) for both its Utah-based Velvet-Wood uranium and vanadium project (“Velvet-Wood”), its Colorado-based Slick Rock uranium and vanadium project (“Slick Rock”) and six of the nine mines which comprise the West Slope complex (“West Slope Mines”). The technical report on the PEA titled, “The Shootaring Canyon Mill and Velvet-Wood and Slick Rock Uranium Projects, Preliminary Economic Assessment”, will be published on SEDAR+ within 45 days from the date of this news release. These eight projects, being Velvet-Wood, Slick Rock and the West Slope Mines, are located proximal to one another within the prolific Uravan Mineral Belt, and within close distance of the Company’s Shootaring Canyon Mill (“Shootaring”) which will act as a centralized mineral processing facility in the PEA. The PEA was prepared in accordance with National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”).

Anfield CEO, Corey Dias, stated, “We are extremely pleased with the outcome of this updated PEA as it provides Anfield with strong further evidence of the true value of the combination of Velvet-Wood, Slick Rock and the West Slope mines within Anfield’s uranium and vanadium hub-and-spoke production model.

Critically, the future potential addition of the Company’s thirteen remaining U.S. Department of Energy leases (“DOE Leases”) to Anfield’s production model pipeline - which will require little incremental capital expenditure - provides significant valuation upside, especially given that Shootaring’s restart costs will have already been borne by initial production from the Velvet-Wood, Slick Rock and West Slope mines.

We have been keen to highlight the economic value of securing increased throughput capacity and production output at Shootaring as we look to leverage our uranium and vanadium assets into one cohesive development project, and the subsequent availability of excess uranium and vanadium production capacity at Shootaring over the life of the mill. We view this increased capacity as providing important additive value through the potential for future integration of other uranium and vanadium projects in the area, such as our other DOE Leases, as well as potential toll-milling opportunities. Finally, the prospect of our largest single uranium mine – Marquez-Juan Tafoya – as an additional source of uranium could further extend the production timeline or provide an incentive to once again expand throughput capacity at Shootaring.

The prospect of Shootaring becoming the second of only two operational conventional uranium and vanadium mill in the United States is significant both economically as well as with respect to security of supply for utilities. This PEA not only represents a significant milestone for Anfield but also outlines a technical and economic path towards commercial development of its core uranium and vanadium assets. Moreover, the Company is currently reviewing a number of other value-added techniques and technologies to facilitate the reduction of waste in order to improve uranium and vanadium grades which can provide the Company with an opportunity to further improve annual production output.

Anfield is well-positioned to benefit from an improving uranium market as nuclear energy becomes critically needed for data centres in the U.S. and as nuclear energy becomes a more integral part of the global transition towards electrification.”

Project Economics

The PEA provides for a 12-month pre-production period. This includes the following capital expenditures, forecasted at approximately US$97 million (including a 20% contingency): (1) initial mill and mine permitting and licensing; (2) an updated mining and reclamation plan; (3) initiation of mine development; (4) completion of the construction of mine facilities and purchasing of equipment; (5) refurbishment of the Shootaring uranium circuit and the construction of a vanadium circuit; and (6) the updating of the tailings waste management facility. An additional US$20 million of mine-related expenditures will occur during the initial production year. The total costs for “Life of Mine” is estimated at US$173 million, including sustaining capital.

The PEA indicates a pre-tax IRR of 106% at a uranium price of US$100 per pound and US$9 per pound of vanadium. The pre-tax NPV of the project at an 8% discount rate at the aforementioned prices is US$606 million. The PEA also indicates a post-tax IRR of 97% and a pre-tax NPV of $533 million.

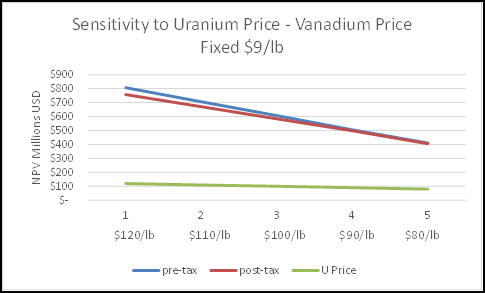

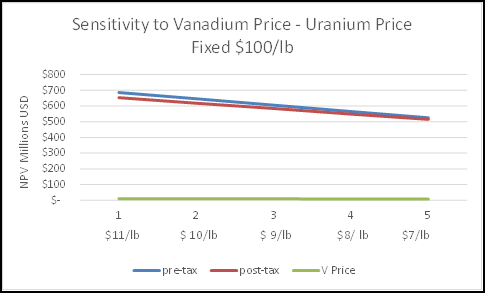

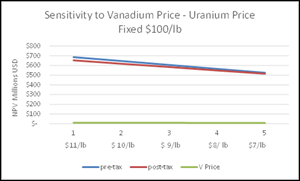

Sensitivity to commodity prices

Changing the commodity price for uranium and vanadium equally by 10% varies the NPV@8% approximately +/- US$136 million pre-tax, and +/- US$117 million post-tax. In both pre-tax and post-tax scenarios the IRR varies by approximately 20% with a 10% variation in price.

Sensitivity to Commodity Price and Discount Rate

| Pre Income tax | NPV @ 0% | $ | 1,090,409 | Pre Income tax | NPV @ 0% | $ | 849,466 | Pre Income tax | NPV @ 0% | $ | 1,331,352 | ||||||||||||

| U Price | $ | 100.00 | NPV @ 5% | $ | 746,476 | U Price | $ | 90.00 | NPV @ 5% | $ | 579,962 | U Price | $ | 110.00 | NPV @ 5% | $ | 912,989 | ||||||

| V Price | $ | 9.00 | NPV @ 8% | $ | 605,633 | V Price | $ | 8.10 | NPV @ 8% | $ | 469,064 | V Price | $ | 9.90 | NPV @ 8% | $ | 742,201 | ||||||

| NPV @ 10% | $ | 530,358 | NPV @ 10% | $ | 409,649 | NPV @ 10% | $ | 651,067 | |||||||||||||||

| Base Case | NPV @ 12% | $ | 466,696 | 10% Price Reduction | NPV @ 12% | $ | 359,317 | 10% Price Increase | NPV @ 12% | $ | 574,075 | ||||||||||||

| IRR | 106 | % | IRR | 85 | % | IRR | 129 | % | |||||||||||||||

| Post Income tax | NPV @ 0% | $ | 964,683 | Post Income tax | NPV @ 0% | $ | 759,239 | Post Income tax | NPV @ 0% | $ | 1,170,128 | ||||||||||||

| U Price | $ | 100.00 | NPV @ 5% | $ | 658,283 | U Price | $ | 90.00 | NPV @ 5% | $ | 515,963 | U Price | $ | 110.00 | NPV @ 5% | $ | 800,604 | ||||||

| V Price | $ | 9.00 | NPV @ 8% | $ | 532,924 | V Price | $ | 8.10 | NPV @ 8% | $ | 415,994 | V Price | $ | 9.90 | NPV @ 8% | $ | 649,854 | ||||||

| NPV @ 10% | $ | 465,957 | NPV @ 10% | $ | 362,476 | NPV @ 10% | $ | 569,438 | |||||||||||||||

| Base Case | NPV @ 12% | $ | 409,342 | 10% Price Reduction | NPV @ 12% | $ | 317,168 | 10% Price Increase | NPV @ 12% | $ | 501,516 | ||||||||||||

| IRR | 97 | % | IRR | 78 | % | IRR | 118 | % | |||||||||||||||

NPV: Sensitivity to Uranium Price

NPV: Sensitivity to Vanadium Price

Source: BRS

Shootaring Mill

The Shootaring area covers approximately 265 acres of surface ownership and approximately 905 acres of mineral leases.

Shootaring was licensed and constructed by Plateau Resources Limited and operated in 1982. U.S. Energy Corp. and Uranium One Inc. were also previous owners of Shootaring. Shootaring has not been decommissioned and has been under care and maintenance since cessation of operations. The mill license has been maintained and Anfield is currently conducting engineering and design studies for both the refurbishment of Shootaring and tailings facility in support of converting the license from its status of care and maintenance to operations.

Velvet-Wood

Velvet-Wood covers approximately 2,140 acres, including unpatented mining claims and a State of Utah mineral lease related to the Velvet-Wood mine areas comprising Velvet-Wood.

Between 1979 and 1984, Atlas Minerals mined approximately 400,000 tons of ore from the Velvet deposit at grades of 0.46% U3O8 and 0.64% V2O5, recovering approximately 4.0 million pounds of U3O8 and 5.0 million pounds of V2O5.

The current mineral resources of the combined Velvet and Wood historical mines have been estimated to comprise 0.63 million tons containing 4.3 million pounds of eU3O8, at a grade of 0.34% eU3O8 (measured and indicated mineral resource), and 80,000 tons containing 544,000 pounds of eU3O8, at a grade of 0.34% U3O8 (inferred mineral resource) with a vanadium-to-uranium ratio of 1.4 to 1.

Slick Rock

Slick Rock Complex is located in the Uravan Mineral Belt region of Colorado and covers approximately 6,130 acres, including 293 unpatented mining lodes claims, and two DOE Leases. The PEA estimates 0.8 million pounds of eU3O8, at a grade of 0.16% eU3O8 (indicated mineral resource) and 2.25 million tons containing 9.1 million pounds at a grade of 0.20% U3O8 (inferred mineral resource) with a vanadium-to-uranium-ratio of 6 to 1.

JD-6, JD-7, JD-8 and JD-9

The JD Mines, located in Colorado, represent four of the nine West Slope mines acquired from Cotter Corporation in late 2018. The PEA estimates 4.6 million pounds of eU3O8, at a grade of 0.22% eU3O8 (indicated mineral resource) with a vanadium-to-uranium-ratio of 5 to 1.

SR-11 and SM-18

The SR-11 and SM-18 mines, located in Colorado, represent two of the nine West Slope mines acquired from Cotter Corporation in late 2018. The PEA estimates 0.16 million tons containing 0.7 million pounds at a grade of 0.24% U3O8 (inferred mineral resource) with a vanadium-to-uranium-ratio of 6 to 1 for SR-11 and 0.18 million tons containing .7 million pounds at a grade of 0.21% U3O8 (inferred mineral resource) with a vanadium-to-uranium-ratio of 5 to 1 for SM-18. Please see resource disclosure for both SR-11 and SM-18 in section titled Mineral Resource Estimate below.

Mineral Resource Estimate

The PEA is based on the mineral resource estimates set forth in the Company’s previous technical reports titled “US DOE Uranium/Vanadium Leases JD-6, JD-7, JD-8 and JD-9, Montrose County, Colorado, USA, Mineral Resource Technical Report, National Instrument 43-101” dated effective April 10, 2022 and “The Shootaring Canyon Mill and Velvet-Wood and Slick Rock Uranium Projects, Preliminary Economic Assessment National Instrument 43-101” dated effective May 6, 2023. There has been no material change in such mineral resource estimates for the Velvet-Wood, Slick Rock, Shootaring and the JD Mines. For the purpose of this PEA, the mineral resource estimates were reviewed by the qualified persons under the PEA and deemed to remain valid and effective.

SR-11 Project Resource Estimate

The SR-11 Project is located approximately 8 miles southwest of the Slick Rock Complex and includes the SR-11 DOE Lease. This lease was previously held and operated by Cotter Corporation into the Mid 2000s. This is the initial resource estimate for the property performed by Anfield. The data set acquired from Cotter Corporation was validated using existing and available geophysical logs. Drilling density would otherwise justify a higher resource classification. However, more field validation of historic drill hole locations or new confirmatory drilling is needed to raise the classification above Inferred.

The existing data for SR-11 consists of 741 drill collars, of which 605 drill holes had associated grade and thickness data. The 136 drill holes without data were limited to the margins of the SR-11 resource area and thus are considered by the authors to have low impact on the data set overall. GT Contour modeling was performed using under the key assumptions described in the table below, and was performed at 0.1ft%, 0.3ft% and 0.5 ft% eU3O8 GT cutoffs for sensitivity analysis. Nominal minimum thickness at the 0.4 ft% GT cutoff is 4 feet. However, lower GT cutoffs would reduce the nominal mining thickness to closer 3ft. Meaning that Jack Leg, room and pillar mining would likely dominate the method of extraction of the SR-11 resource.

The minimum sum GT contour resource model cutoff is the primary cutoff criteria applied to the contour model volume as the initial screening of those portions of the model quantities not meeting the criteria for reasonable economic extraction. In addition, individual model areas outside the conceptual mine limits not meeting a minimum of 10,000 lbs of eU3O8 resource were excluded from the resource totals as not meeting a minimum expectation of reasonable economic extraction. It is the opinion of the authors of the PEA that the resource models are reasonably valid within the mineral resource classifications assigned to each area of the complex.

A sensitivity analysis was performed on the mineral resource models for each zone as shown in the table below. The authors recommend the 0.40 GT cutoff for the SR-11 Project. With further definition of the mineral resource via drilling and additional mine design and cost evaluation, it is the authors’ opinion that the minimum GT cutoff may be lowered with appropriate adjustments to mining methods made.

Inferred Mineral Resources Uranium, SR-11 Lease

| Zone / Classification | GT Cutoff (ft%) | AVG. Thickness (ft) | AVG. Grade (%eU3O8) | Tons | Pounds (eU3O8) |

| SR-11 / Total Inferred | 0.1 | 3.2 | 0.15 | 361,217 | 1,064,700 |

| 0.25 | 3.6 | 0.20 | 229,039 | 909,504 | |

| 0.4 | 3.9 | 0.24 | 163,480 | 774,360 | |

Mineral resources are not mineral reserves and do not have demonstrated economic viability in accordance with the Canadian Institute of Mining, Metallurgy and Petroleum standards. At a minimum, a preliminary feasibility study is required to demonstrate the economic viability of the measured and indicated mineral resources and qualify an initial estimate of mineral reserves. The PEA is preliminary in nature such that it includes a portion of the inferred mineral resources. Inferred mineral resources are too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the outcomes estimated in the PEA will be realized.

SM-18 Project Resource Estimate

The SM-18 Project within the SM-18 DOE Lease, located approximately 11 miles north of the Paradox Complex. This lease was previously held and operated by Cotter Corporation into the Mid 2000s. This is the initial resource estimate for the property performed by Anfield. The data set acquired from Cotter Corporation was validated using existing and available geophysical logs. Drilling density would otherwise justify a higher resource classification. However, more field validation of historic drill hole locations or new confirmatory drilling is needed to raise the classification above Inferred.

The existing data for SM-18 consists of 681 drill collars, of which 677 drill holes had associated grade and thickness data. The 4 drill holes without data were limited to the margins of the SM-18 resource area and thus are considered by the authors of the PEA to have low impact on the data set overall. GT Contour modeling was performed using the key assumptions described in the table below, and was performed at 0.1ft%, 0.3ft% and 0.5 ft% eU3O8 GT cutoffs for sensitivity analysis. Nominal minimum thickness at the 0.4 ft% GT cutoff is 4 feet.

The minimum sum GT contour resource model cutoff is the primary cutoff criteria applied to the contour model volume as the initial screening of those portions of the model quantities not meeting the criteria for reasonable economic extraction. In addition, individual model areas outside the conceptual mine limits not meeting a minimum of 10,000 lbs of eU3O8 resource were excluded from the resource totals as not meeting a minimum expectation of reasonable economic extraction. It is the opinion of the authors that the resource models are reasonably valid within the mineral resource classifications assigned to each area of the complex.

A sensitivity analysis was performed on the mineral resource models for each zone as shown in the table below. The authors recommend the 0.40 GT cutoff for the SR-11 Project. With further definition of the mineral resource via drilling and additional mine design and cost evaluation, it is the authors’ opinion that the minimum GT cutoff may be lowered with appropriate adjustments to mining methods made.

SM-18 Project Inferred Mineral Resource Estimates by GT Cutoff

| Zone | GT Cutoff (ft%) |

AVG Thickness (ft) |

AVG. Grade (%eU3O8) |

Tons | Pounds (eU3O8) |

| A | 0.1 | 3.2 | 0.112 | 574,325 | 1,286,280 |

| 0.25 | 4.1 | 0.152 | 325,058 | 985,779 | |

| 0.4 | 4.2 | 0.211 | 178,965 | 755,367 | |

| Total | 0.1 | 3.2 | 0.112 | 574,325 | 1,286,280 |

| 0.25 | 4.1 | 0.152 | 325,058 | 985,779 | |

| 0.4 | 4.2 | 0.211 | 178,965 | 755,367 | |

While no formal economic evaluation, preliminary economic assessment, preliminary feasibility study, or feasibility study has been completed and while mineral resources are not mineral reserves and do not have demonstrated economic viability, reasonable prospects for future economic extraction were applied to the mineral resource estimate herein through consideration of grade and GT cutoffs and by screening out areas of isolated mineralization which would not support the cost of conventional mining under current and reasonably foreseeable conditions.

NI 43-101 Disclosure

The combined PEA completed for Velvet-Wood, Slick Rock and the West Slope Mines, using centralized processing at Shootaring, has been authored by Terence (Terry) McNulty, P.E., D. Sc., of T.P. McNulty and Associates Inc. and co-author Douglas L. Beahm, P.E. PG. Dr. McNulty is independent of the issuer in accordance with the application of Section 1.5 of NI 43-101. Mr. Beahm is not independent of the Company, as he is the Company’s Chief Operating Officer. The authors have reviewed and verified that the scientific and technical content of this news release in respect of the PEA is accurate and approve the written disclosure of such information.

Additional scientific and technical information in this news release not specific to the PEA has been prepared under the supervision of and approved by Douglas L. Beahm, P.E., P.G., a qualified person as defined by NI 43-101, and Mr. Beahm has reviewed, verified and approved such scientific and technical information contained in this news release. No limitations or failures to verify were identified. Mr. Beahm is not independent of the Company, as he is the Company’s Chief Operating Officer.

Results of the PEA represent forward-looking information. The PEA is preliminary in nature and it includes inferred mineral resources that are considered too speculative, geologically, to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the PEA will be realized. There is no guarantee that inferred mineral resource estimates will be converted to indicated or measured mineral resources, or that indicated or measured mineral resources can be converted to mineral reserves. Mineral resources that are not mineral reserves do not have demonstrated economic viability, and as such there is no guarantee the project economics described herein will be achieved. Mineral resource estimates may be materially affected by environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant risks, uncertainties and other factors, as more particularly described herein and to be described in the technical report in respect of the PEA.

Conditions and parameters of the project are subject to change based on the final filing of the PEA on SEDAR+ within 45 days of this release. Further information about the PEA referenced in this news release, including information in respect of data verification, key assumptions, parameters, risks and other factors, will be contained in a technical report, which will be filed by the Company in respect of the PEA within 45 days under its profile at SEDAR+ at www.sedarplus.ca. Readers are encouraged to read the technical report in its entirety, including all qualifications, assumptions and exclusions that relate to the PEA. The technical report is intended to be read as a whole, and sections should not be read or relied upon out of context.

Non-IFRS Financial Measures

The Company has included certain non-IFRS financial measures in this news release, such as sustaining capital, which is not a measure recognized under IFRS and does not have a standardized meaning prescribed by IFRS. As a result, this measure may not be comparable to similar measures reported by other companies. This measure used is intended to provide additional information to the reader and should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. The non-IFRS financial measure used in this news release is defined below.

Sustaining Capital is a supplementary financial measure and defined as cash-basis expenditures which maintain operations and sustain production levels.

The projects that are subject of this news release do not currently have operations and therefore do not have historical equivalent measures to compare to. As such, the Company cannot perform a reconciliation of this non-IFRS measure.

About Anfield

Anfield is a uranium and vanadium development company that is committed to becoming a top-tier energy-related fuels supplier by creating value through sustainable, efficient growth in its assets. Anfield is a publicly traded corporation listed on the NASDAQ (AEC-Q), the TSXV (AEC-V) and the Frankfurt Stock Exchange (0AD).

On behalf of the Board of Directors

ANFIELD ENERGY INC.

Corey Dias, Chief Executive Officer

Neither the TSXV nor its Regulation Services Provider (as that term is defined in policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

Contact:

Anfield Energy, Inc.

Corporate Communications

604-669-5762

contact@anfieldenergy.com

www.anfieldenergy.com

This news release contains forward-looking statements and forward-looking information (together, “forward-looking statements”) within the meaning of applicable Canadian securities laws. All statements, other than statements of historical facts, are forward-looking statements. Generally, forward-looking statements can be identified by the use of terminology such as “plans”, “expects”, “estimates”, “intends”, “anticipates”, “believes” or variations of such words, or statements that certain actions, events or results “may”, “could”, “would”, “might”, “occur” or “be achieved”. Forward-looking statements in this release include, but are not limited to, statements regarding the timing of completion of a technical report summarizing the results of the PEA; the development, operational and economic results of the PEA, including capital expenditures, NPV projections, IRR projections, development costs and sustaining capital; the plans for Shootaring to serve as a centralized mineral processing facility; estimation of future production; the potential of Velvet-Wood, Slick Rock, JD-7 and JD-8 within the Company’s uranium and vanadium hub-and-spoke production model; the potential addition of the Company’s 13 remaining DOE Leases to the Company’s production model pipeline and the expected capital expenditures needed; the Company’s plan to secure increased throughput capacity and production output at Shootaring; the availability of excess uranium and vanadium production capacity at Shootaring over the life of the mill and benefits therefrom; the potential future integration of other uranium and vanadium projects in the area of Shootaring; the potential of the Marquez-Juan Tafoya mine as an additional source of uranium to further extend the production timeline; the prospect of Shootaring becoming the next operational conventional uranium and vanadium mill in the United States and the benefits therefrom; the commercial development of the Company’s core uranium and vanadium assets; the Company’s usage of value-added techniques and technology to reduce waste in order to improve uranium and vanadium grades and further improve annual production output; the uranium market and the trend of nuclear energy becoming integral to the global transition towards electrification and the expected benefits therefrom; the conversion of the Shootaring license from its status of care and maintenance to operations and the economics and viability of development of Velvet-Wood, Slick Rock and the West Slope Mines.

Forward-looking statements involve risks, uncertainties and other factors that could cause actual results, performance and opportunities to differ materially from those implied by such forward-looking statements. Factors that could cause actual results to differ materially from these forward-looking statements include, among other things: risks that the technical report may not be completed as contemplated, or at all; risks that the development, operational and economic results of the PEA may differ from projections; risks that the potential of Velvet-Wood, Slick Rock, JD-7 and JD-8 within the Company’s uranium and vanadium hub-and-spoke production model may not be realized as contemplated, or at all; risks that the Company may not add its 13 remaining DOE Leases to the Company’s production model pipeline as contemplated, or at all; risks that the expected capital expenditures needed to add the 13 DOE Leases to the production model pipeline may vary from current expectations; risks that the Company may not be able to secure increased throughput capacity and production output at Shootaring as contemplated, or at all; risks that excess uranium and vanadium production capacity at Shootaring over the life of the mill may not be available as contemplated, or at all; risks that the integration of other uranium and vanadium projects in the area may not be completed as contemplated, or at all; risks that the potential of the Marquez-Juan Tafoya mine as an additional source of uranium to further extend the production timeline may not be realized as contemplated, or at all; risks that the Shootaring may not become an operational conventional uranium and vanadium mill in the United States as contemplated, or at all; risks that the commercial development of the Company’s core uranium and vanadium assets may not be completed as contemplated, or at all; risks that the anticipated benefits of the Company’s usage of value-added techniques and technology to reduce waste in order to improve uranium and vanadium grades may not be realized as contemplated, or at all; risks related to the global uranium market; risks that nuclear energy may not become integral to the global transition towards electrification as contemplated; risks that the Company may not successfully convert the status of the mill license for Shootaring from care and maintenance to operations as contemplated, or at all; risks related to the economics and viability of development of Velvet-Wood, Slick Rock and West Slope Mines; the risks and uncertainties relating to exploration and development; the ability of the Company to obtain additional financing; the need to comply with environmental and governmental regulations in Canada and the United States; fluctuations in the prices of commodities; operating hazards and risks; competition and other risks and uncertainties and other such factors as are set forth in the annual information form for the Company’s most recently completed year end, as well as the management discussion and analysis and other disclosures of risk factors for the Company, filed on SEDAR+ at www.sedarplus.ca.

Although the Company believes that the information and assumptions used in preparing the forward-looking statements are reasonable, undue reliance should not be placed on these statements, which only apply as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. Except where required by applicable law, the Company disclaims any intention or obligation to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

Photos accompanying this announcement are available at:

https://www.globenewswire.com/NewsRoom/AttachmentNg/613d88f5-f657-468f-86de-b9682a765392

https://www.globenewswire.com/NewsRoom/AttachmentNg/f7149648-a59e-44ae-875a-2c157c4af89d

NPV: Sensitivity to Uranium Price

Source: BRS

NPV: Sensitivity to Vanadium Price

Source: BRS

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.